The International Council on Clean Transportation (ICCT) has released a study outlining the CO2 reduction requirements for the ten largest car manufacturers to comply with the European Union’s fleet limits set for 2025. On average, manufacturers will need to increase their battery electric vehicle (BEV) share by up to twelve percentage points, raising it from 16 percent in 2023 to approximately 28 percent by 2025.

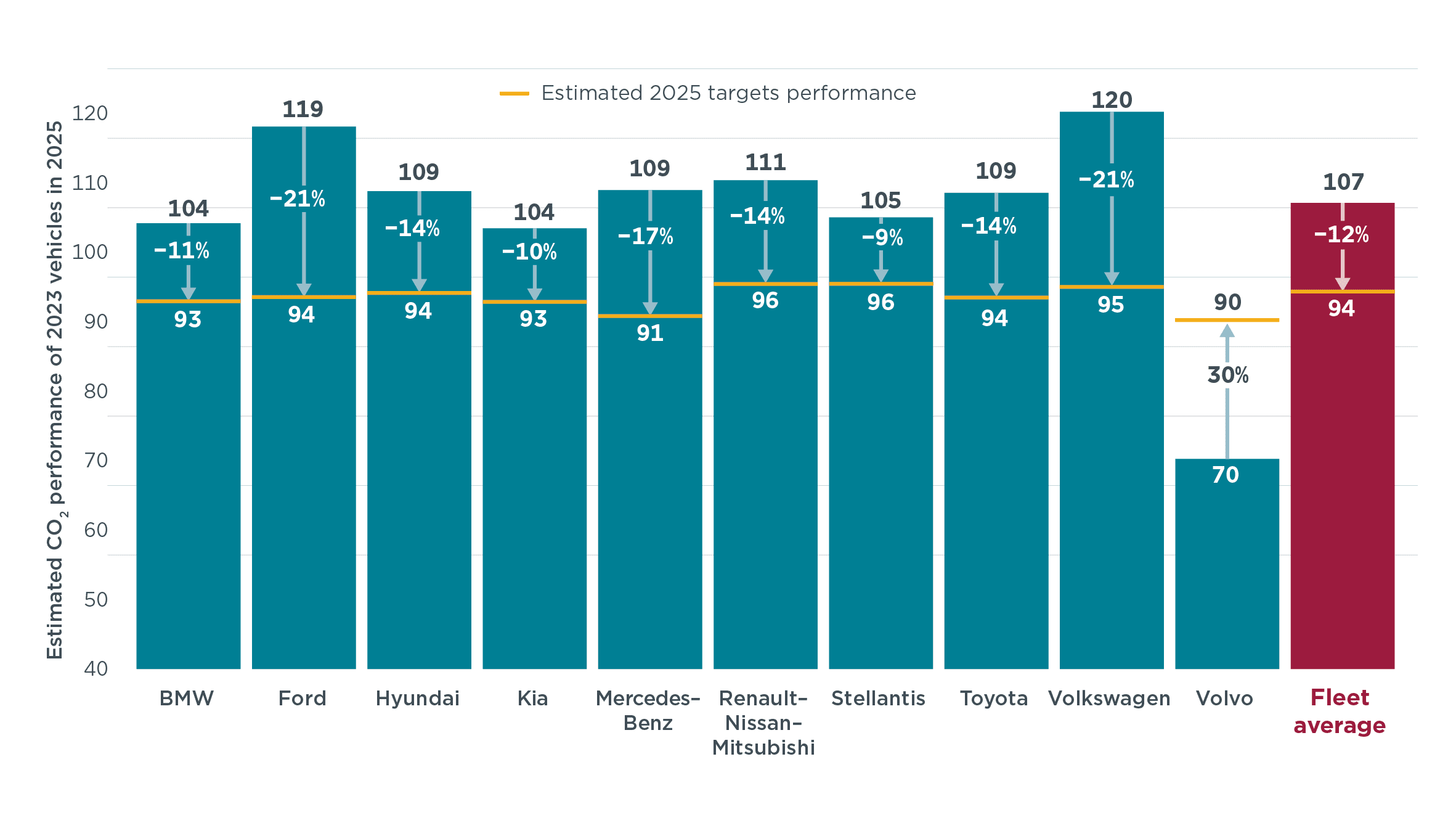

According to the ICCT survey, Volkswagen and Ford face the most significant challenges, with required CO2 reductions of around 21 percent. Hyundai, Mercedes-Benz, and Toyota are also required to reduce their emissions beyond the average threshold. In contrast, BMW, Kia, and Stellantis are positioned closest to their targets, needing reductions of between nine and eleven percent.

The ICCT’s findings align with a prior study by Dataforce, published in August, which also identified Volkswagen and Ford as the two manufacturers requiring the most considerable effort to meet their targets of 123 and 125 g/km of CO2 emissions, respectively. However, the two studies diverge in certain assessments; for instance, Dataforce found Toyota, Hyundai, BMW, and Mercedes-Benz to be closely grouped, while Stellantis and Renault-Nissan-Mitsubishi were placed in a middle tier.

2025 Manufacturer CO2 targets versus 2023 fleet performance

Notably, the ICCT and Dataforce studies differ in their evaluations of specific manufacturers. The ICCT reported a one-gram difference for Mercedes-Benz between the two studies, while Stellantis is assessed to perform better in the ICCT study, with emissions of 105 grams instead of 113 grams, significantly affecting its required proportion of electric vehicles. For Renault-Nissan-Mitsubishi, the discrepancy is as much as three grams.

Using the current CO2 fleet emissions and individual manufacturer targets for 2025, the report outlines potential shifts in drive technology distributions for each company. For instance, while Volvo would not need to alter its strategy, the Volkswagen Group would need to increase its BEV sales from 13 percent in 2023 to 30 percent. This shift would correspond with a decrease in combustion engine sales from 81 to 64 percent, assuming a steady plug-in hybrid electric vehicle (PHEV) share of six percent. Conversely, Toyota, despite its efficient combustion engines, has a lower share of electric vehicles and would need to raise its BEV percentage from three to 16 percent, as calculated by the ICCT. BMW is projected to increase its EV share from 20 percent in 2023 to 27 percent next year.

The ICCT study underscores that quantifying the exact BEV share each manufacturer must achieve to meet fleet limits is complex. The report notes, “Besides increasing their BEV sales share, compliance flexibilities within the legislation, technological progress, and adjusted marketing strategies offer manufacturers additional options to meet the targets.” The study concludes that the 2025 targets are attainable, considering the previous CO2 reductions achieved by manufacturers.

Maximum BEV share required by manufacturers in 2025 to meet their CO2 targets

Peter Mock, Head of Europe at ICCT, remarked that the analysis is “a very conservative analysis, worst-case, so to speak. In reality, the BEV shares will be lower because the OEMs will also resort to other measures (and tricks).” Manufacturers have alternatives, such as increasing sales of PHEVs or more efficient combustion-engine vehicles, which could lead to fewer BEVs needing to be sold to meet CO2 emissions targets. Additionally, manufacturers can form CO2 pools with others, allowing those who exceed their targets to partner with those who do not.

Regardless of the strategies employed, the study concludes that achieving the CO2 targets for 2025 is feasible, taking into account past emissions reductions, regulatory flexibility, and the available drive technologies. “The CO2 reductions needed is about half of previous reductions achieved by manufacturers,” the report states, highlighting that manufacturers reduced emissions by 23 percent between 2019 and 2021, indicating that a 12 percent reduction between 2023 and 2025 is achievable. The required increase in BEV market share for hypothetical manufacturer pools is estimated to be “about 1–1.5 times as high as the growth observed from 2019 to 2021,” according to the ICCT.

Source: theiict.org