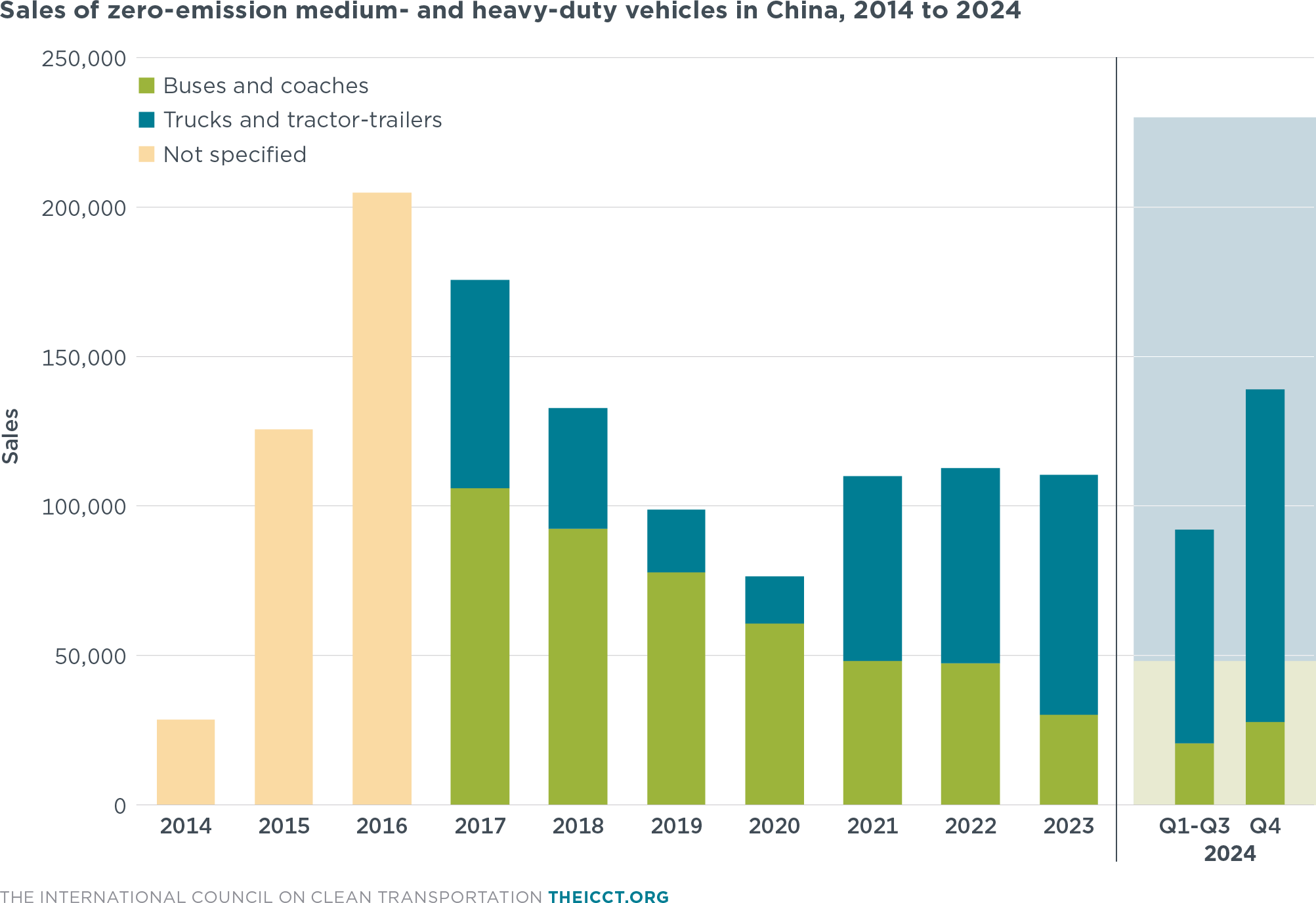

Sales of zero-emission trucks and buses in China soared to a record 230,000 units in 2024, driven by a robust macroeconomic stimulus package released by the government in September, according to a new analysis by the International Council on Clean Transportation (ICCT). The surge marked the highest level since the previous peak of 200,000 units in 2015–2016, which had been fueled by government incentives.

“China’s zero-emission truck and bus market experienced significant growth in 2024, particularly in the fourth quarter following the government’s macroeconomic stimulus package,” said Felipe Rodríguez, ICCT Heavy-Duty Vehicle Program Director and co-author of the analysis. “The increasing market maturity and manufacturer consolidation suggest that zero-emission technologies are becoming mainstream in China’s commercial vehicle sector. A decade of ambitious policies has driven a transformative shift, positioning manufacturers well for the rapid growth that upcoming regulations, like China VII, will spur.”

Battery electric vehicles dominated the zero-emission market, accounting for 13% of medium truck sales and 14% of heavy truck sales. Fuel cell trucks, however, remained a nascent technology, representing less than 1% of the heavy truck segment. The heavy truck market share surged to nearly 21% in December, more than doubling its January levels, while medium trucks reached 22%, nearly tripling their January share.

City bus electrification in China had already reached full market penetration by 2023, with nearly 100% of sales comprising battery electric, hybrid electric, and fuel-cell electric models. In contrast, battery electric coaches used for intercity transport accounted for only 6% of market share in 2024.

The zero-emission heavy truck market saw increasing consolidation, with the top five manufacturers—XCMG, SANY, FAW, Shacman, and Yutong—capturing 61% of sales. This level of market concentration approached that of internal combustion engine (ICE) truck manufacturers, which held a 75% share.

Battery swapping technology gained traction in 2024, with sales of swap-capable vehicles rising 94% year-on-year to 29,569 units. Policy incentives and industry demand, particularly in mining, steel, and port logistics, contributed to this growth.

The zero-emission medium- and heavy-duty vehicle (ZE-MHDV) market has experienced two major spikes over the past decade: first in 2015–2016, driven by government subsidies, and again in 2024 following the stimulus package. In 2024, trucks and tractor-trailers accounted for approximately 80% of ZE-MHDV sales, highlighting the industry’s shift towards zero-emission solutions for freight transport. Meanwhile, bus and coach sales declined, reflecting market saturation after years of policy-driven electrification efforts.

The heavy truck market saw a shift in powertrain distribution. Diesel trucks accounted for 57% of sales in 2024, down from 70% in 2023, while natural gas trucks held a 29% market share. Battery electric trucks climbed to 13%, making them the third most popular powertrain. Sales of battery electric and fuel-cell heavy trucks steadily increased throughout the year, apart from a February dip due to the Spring Festival. In December, battery electric heavy truck sales reached over 14,700 units, capturing a 20.9% market share—more than double January’s level. Fuel-cell heavy truck sales remained limited, with 581 units sold in December, representing 0.8% of the market.

Lithium iron phosphate (LFP) batteries dominated China’s heavy truck market. The most common battery sizes were 282 kWh, 350 kWh, and 423 kWh, reflecting a balance between cost and operational efficiency. Among medium battery electric trucks, LFP batteries also prevailed, with most models equipped with 50 kWh to 100 kWh packs.

Market concentration among leading manufacturers remained tight. The top five ICE heavy truck OEMs—FAW, Dongfeng Motor, Foton-Daimler, Shaanxi Auto, and Sinotruk/CNHTC—held a combined 75% market share. In comparison, the top five zero-emission truck manufacturers—XCMG, SANY, FAW, Hunan Truck, and Shaanxi Auto—captured 54% of the segment. This suggests that the zero-emission truck market is maturing and catching up to ICE truck dominance.

City buses led electrification efforts, with nearly 100% of the market comprising battery electric, hybrid electric, and fuel-cell electric models as of 2024. In contrast, battery electric coaches represented just 6% of sales. City bus sales peaked in December at over 17,000 units, with battery electric models making up approximately 99% of purchases. The increase was largely due to incentives for replacing older electric buses and batteries, which were set to expire at year-end. Battery electric coach market share reached a 2024 high of 12% in December, while fuel-cell coach sales remained marginal, peaking at 247 units in August.

Battery swapping technology saw increased adoption, particularly for trucks and tractors. Fleet operators benefited from lower upfront costs by purchasing vehicles without pre-installed batteries and leasing them instead. The presence of swap infrastructure enabled continuous operation by minimizing charging downtime.

Sales of swap-capable vehicles surged in 2024 to 29,569 units, a 94% increase over the previous year. Government policies and pilot projects in industries such as mining, steel, and port logistics played a crucial role in driving demand.

Natural gas-powered trucks have also gained traction in China since 2023, driven by factors including the lifting of COVID-19 transport restrictions and increased natural gas imports, which lowered fuel costs. Sales peaked in September 2023 and March 2024, coinciding with favorable shifts in fuel prices. However, concerns persist regarding their environmental impact, as natural gas trucks produce significant nitrogen oxide emissions and contribute to methane leakage. While viewed as a cleaner alternative to diesel, their overall emissions benefits remain limited.